The Zeroth World: A Seven-Year Update

TL;DR: Seven years ago I argued that AI could enable a zeroth world: economies operating at a multiple of first-world productivity, the way the first world operates at a multiple of the third. The update: the technology arrived faster than I expected, the productivity gains are real but unevenly distributed, and the zeroth world is being built right now, in the US and in China. Europe is perfectly on track to watch from the sidelines, which is particularly bitter because, demographically, Europe needs it more than anyone else. The newest twist: frontier cyber-defense capability is now allocated by invitation and Europe is mostly not on the list.

Note for German readers: there is a full German version of this post at the bottom, AI-generated with zero touch-ups; take it or leave it.

Hinweis für deutsche Leser: Ganz unten gibt es eine vollständige deutsche Version dieses Beitrags, KI-generiert und ohne jede Nachbearbeitung; take it or leave it.

In my previous post on the zeroth world, I discussed the impact of artificial intelligence on society and the economy, emphasizing its current and latent capabilities rather than speculative future scenarios. I defined AI as systems that gather information, learn, decide, and act autonomously, similar to the OODA loop. I highlighted the need for hybridization, where AI systems teamed up with humans to enhance productivity and scale operations. Examples included autonomous driving, call center operations, and investment portfolio management. I also explored the potential for AI to create a “Zeroth World” with unprecedented economic output and productivity levels; basically, the zeroth world is to the first world what the first world is to the third world in terms of economic output. I also discussed to some extent the risks of job displacement and the concentration of power.

That was seven years ago, written while I was still living in the US, before relocating to Europe (Germany to be more precise). A lot has happened since then and this is the update. Full disclosure: I started writing the update on January 28, 2025 (it was meant to be a six-year update), the week DeepSeek R1 dropped. It then sat in my drafts folder for almost a year and a half, during which everything in it became more true.

The backdrop to finally shipping the post is too obvious to ignore: Today, 12th of June 2026, SpaceX is going public after raising $75 billion at a roughly $1.8 trillion valuation, the largest IPO in history and about two and a half times Saudi Aramco’s old record; Anthropic and OpenAI filed to follow within the same two weeks. With this the zeroth world is now a tradeable asset class.

NOTE. Stating the obvious or the most likely outcome is not an endorsement.

What the 2019 post got right (and wrong)

Before making a new set of predictions for the future, let us settle my old ones from 2019 first.

What hit:

- Hybridization was the right call. The 2019 thesis was that we do not need full autonomy, we need a human paired with an AI handling “90% of the basics with human override”. That is, almost verbatim, the deployment pattern of 2023-2026: copilots, assistants, agents with escalation. Klarna’s assistant took over two-thirds of customer-service chats in its first month, the workload of several hundred agents. The best-studied call-center deployment showed ~14% average productivity gains, ~34% for novices. Call centers were literally the first example on my 2019 list.

- The control-center driving model. In 2019 I sketched two use cases: remote operators supervising multiple vehicles, and hub-to-hub highway autonomy for trucking. Waymo now does 500,000 paid robotaxi rides per week across ten US cities (with a stated target of a million per week by end of 2026), supported by exactly the kind of remote fleet-assistance layer described back then. Aurora started driverless freight runs between Dallas and Houston in 2025, hub-to-hub, exactly as sketched. And my favorite footnote: teledriving, the purest form of the control-center idea, is offered commercially by Vay… a company founded in Berlin, operating in Las Vegas. Remember that one for later.

- “In a few years you will download such a bot in the App Store.” ChatGPT launched in November 2022, three and a half years after that sentence, and became the fastest-adopted consumer application in history. The companion prediction, that we would soon teach building such systems end-to-end at universities as senior-design projects, is now just called the curriculum.

- Concentration of power. The 2019 post speculated that “the next category of scale will be defined by AI companies, with an insane concentration of resources, wealth, and power that pales current concentration levels in the valley.” NVIDIA became the first $4 trillion company; a handful of US firms now spend on the order of half a trillion dollars per year on AI infrastructure; the top of the S&P 500 is, functionally, an AI index. And as of this week, the “next category of scale” has tickers: SpaceX’s record listing makes it one of the largest companies in America on day one, with OpenAI and Anthropic filed right behind it, roughly four trillion dollars of zeroth-world equity heading for the public markets at once. I will take that one.

- The compute trend. The “3.5-month doubling” of training compute obviously could not continue at that exact rate (every exponential is a sigmoid), but the underlying point, that we were moving faster than any prior technology cycle, held. Training compute for frontier models kept growing at multiples per year, financed by the capex numbers above.

What missed:

- The mechanism. I was watching reinforcement learning and self-play (AlphaStar et al.). The actual breakthrough came from self-supervised learning on text at scale. The shape of the prediction (capability via compute scaling, no fundamental roadblock) was right; the mechanism was not. I count that as lucky in the way that matters and wrong in the way that doesn’t.

- Timelines for the physical world. Driving took longer than the disengagement-rate extrapolation suggested (though it did arrive). Robo-advisors stayed mediocre. Atoms remain harder than bits.

- The aggregate numbers (so far). You still cannot see the zeroth world in GDP statistics. Productivity statistics move slowly, diffusion is lumpy, and we are early. This is the classic Solow problem “computers everywhere except in the productivity statistics”. What you can already see is divergence between blocs, and that is the actual subject of this update.

Agents: the OODA loop par excellence

Re-reading the 2019 definition of an AI system, (1) senses, (2) learns, (3) decides, (4) acts, with some autonomy, it is hard not to smile: that is simply a description of a 2026 agent. Tool use, computer use, coding agents, deep-research agents: the OODA loop commercially at scale. What was an abstraction borrowed from military doctrine is now a product category.

And the productivity gains are real, if uneven. I will not review the vast amount of studies here beyond two calibration points: novice-heavy, well-scoped work shows large gains (the call-center numbers above), while METR’s 2025 study found experienced open-source developers were actually slower with AI tools on their own familiar codebases, while believing they were faster. Both results are true; the distribution of gains is the key point. My own experience, see the The Agentic Researcher post, is that with verification-first workflows the gains in research work are very substantial; and for good measure to balance perspectives, not every discovery needs an LLM.

One of the main hypotheses from 2019 was the automate-and-elevate cycle: automate the basics, operate one level higher, repeat. This is real now, with appropriately scoped and tooled agents. The individual contributor of 2026 increasingly behaves like a manager of processes that happen to in silico; being basically a solo-entrepreneur. That was the mechanism by which I argued a 10x in output per person becomes plausible. I see no reason to retract that claim, rather to ask where it will happen and whether it will compound. Which brings us to the actual update.

The race is between blocs now: US, China, Europe

In 2019 I framed the zeroth world in terms of countries pulling away on GDP per person employed. In 2026, the better way to resolve things is in blocs, because the inputs that matter are bloc-level: compute, energy, data, regulation, capital, talent.

| Factor | US | China | Europe |

|---|---|---|---|

| Frontier compute | ✓✓ | ~ (constrained, compensating, changing fast though) | ✗ |

| Energy (price & buildout) | ~ (cheap, grid-limited) | ✓✓ | ✗ |

| Data | ✓ | ✓✓ | ✗ (by design) |

| Regulation (for builders) | ✓ | ✓ (pragmatic) | ✗ |

| Capital | ✓✓ | ✓ | ✗ (exists, risk-averse) |

| Talent | ✓✓ (imports) | ✓✓ (volume) | ✓ (exports) |

The US is playing the closed frontier game: a handful of labs, essentially unlimited capital, and compute buildouts that have crossed from “data center” into “industrial program”. Stargate was announced at $500 billion the very week I started this draft; xAI’s first Memphis cluster, which I originally cited at 100k GPUs as an outrageous number, passed 200k and the successor site is marketed in gigawatts rather than chip counts. The binding constraint in the US is no longer money or chips; it is electricity and interconnects.

China is playing the open and deployed game, and the DeepSeek moment was not a one-off. Qwen, Kimi, GLM, MiniMax: the most-used open-weight models in the world are now, by a comfortable margin, Chinese, which means the default substrate for everyone outside the frontier labs is increasingly Chinese. Compute is the constraining input (export controls work, partially), but the response has been efficiency engineering plus a domestic accelerator stack maturing fast. And the effort goes all the way down the stack: Reuters has documented a state-orchestrated “Manhattan Project” centered on Huawei to replicate the chip-making toolchain itself, up to and including the one machine everyone agreed was un-replicable, ASML’s EUV lithography. Domestic EUV prototypes are reportedly under testing, with AI-chip output targeted for 2028 (insiders say 2030; analysts used to say a decade). Discount the boasts as you like, serious assessments do, but the direction is unambiguous: the chokepoint is being engineered around. Europe should sit with that for a moment, because ASML in Veldhoven is the continent’s single genuine piece of AI-relevant leverage, and the countdown to end this leverage has started. On energy, there is no contest: China added more generating capacity last year than Germany operates in total, it installed more than twice as much solar in the first half of 2025 as the rest of the world combined, and its cumulative solar fleet crossed the terawatt mark in 2025, much of it in desert megabases like the Kubuqi “Solar Great Wall”, the kind of infrastructure you can watch grow from space. And crucially, China dominates the layer where zeroth-world productivity touches the physical economy: industrial robots (roughly half of global installations), EVs, batteries, electrified manufacturing. If the US owns the brains, China owns the metabolism.

Europe is playing the customer game while describing it as the values game. The EU AI Act entered into force in 2024; by November 2025 the Commission was already proposing, via the digital omnibus, to delay and soften the very rules it had just finished celebrating, after the predictable realization that they were unimplementable. Regulate first, retreat later, build never. On compute, Europe’s proudest machine, JUPITER in Jülich (Europe’s first exascale system, roughly 24k superchips), is a fine scientific instrument and a rounding error against a single US site. The headline response, InvestAI with €200 billion and “AI gigafactories”, remains, as of this writing, largely a press-release asset class. The Draghi report said everything that needed saying in September 2024, in officialese, with numbers; remarkably little has happened since. Mistral exists and is genuinely good, which makes it the exception that proves the rule; Aleph Alpha, the German frontier hope, pivoted out of the frontier race in 2024.

The absorbing state seems obvious: the zeroth world will not be a country club you can apply to join. It is shaping up as two ecosystems, a US-led closed frontier and a China-led open/deployment stack, plus customers. Europe is currently choosing, with great procedural diligence and the unwavering exactness of bureaucracy, to be a customer.

And being a customer, it turns out, now comes in tiers as well.

The Glasswing asymmetry: security by invitation

In April 2026, Anthropic announced Project Glasswing, an initiative to “secure the world’s most critical software”, built around early access to its newest frontier model, Claude Mythos Preview. The model’s defining capability is finding and fixing software vulnerabilities at machine speed; it had “already identified thousands of zero-day vulnerabilities across critical infrastructure” at announcement, and within weeks the launch partners reported more than 10,000 high- or critical-severity flaws found in their codebases. Now think about this for a second: the find-and-fix loop of cybersecurity now runs at AI speed, the window from vulnerability to exploit shrinks from months to minutes, and the same class of capability will be in attackers’ hands roughly one open-weight release cycle later. Everyone’s exposure clock started ticking at once: but who gets hardened first?

The eleven named launch partners: Amazon Web Services, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorganChase, the Linux Foundation, Microsoft, NVIDIA, Palo Alto Networks; not just America first but exclusive. The expansion to roughly 150 further organizations in fifteen-plus countries was decided, in Anthropic’s own words, “following several weeks of close collaboration” with partners, the security industry, open-source maintainers, and the US government. Individual European organizations do get in (BT joined in June, in an expansion round, after meeting Anthropic’s security requirements), but invitation-by-exception is the point here: access to the defensive frontier is discretionary, revocable, and runs through San Francisco and Washington. Privileged access has become industrial policy and hardening is (a new layer of) export control. Nobody banned Europe from anything, they just ended up last in line.

For the zeroth-world narrative this adds a second dimension. The first dimension was productivity; this one is exposure. The US is using frontier AI to systematically harden its own stack first: its clouds, its chips, its banks, its open-source substrate. Europe runs on much of that same software, so it inherits patches downstream, on the vendors’ schedule and according to the vendors’ priorities. But Europe’s own stack, the SAPs and the Siemens control systems, the utilities, the hospital IT, the government systems, the long tail of European code produced in fragmented sovereignty-knee-jerk-reactions, that nobody in Memphis cares about, has no seat at that table and no access to frontier hardening capabilities. No problem, just do your own Project Glasswing in Europe? Europe cannot simply run its own Glasswing, because a Glasswing requires a Mythos, and Europe has no frontier model to gate in order to create such a hardening advantage. Put differently, the capability gap turned into a security gap and there is basically no fix to this.

What is also worth noting is that this episode is more illuminating than a decade of sovereignty white papers outlining hypotheticals; comically, so much has been written and yet no one saw this one coming. While Europe spent years drafting horizontal AI regulation, the actual allocation of AI-era security, arguably the most sovereignty-relevant resource there is, happened via a partner list assembled by a private American company in consultation with its home government, in a matter of weeks. That is what shaping the technology looks like when you are at the table. And this is the definition of being an NPC (not even occuring as an afterthought) if you are not.

Why Europe is never going to catch up in the AI race

I will use Germany as my running example here, partly because I know the system (and live here) and partly because Germany is the largest economy of the bloc and directionally representative; the argument transfers to most others the continent with minor touch-ups.

Let’s start with a quick time capsule moment: On January 28, 2025, when I started this draft, DeepSeek had just released its open models (V3, R1, Janus-Pro), bringing Chinese models up to par with the best in the West, trained on export-controlled, dumbed-down GPUs at a fraction of the usual price point. It sent the stock market spiraling down (“AI in the US is doomed”) just to recover most of it the next day (“wait a sec, cheaper AI means more users and more users means more money”); same story as with the steam engines. Someone sent me a meme that week that still summarizes the situation:

Figure 1: A summary of the state of AI in Germany, and more broadly in Europe. Unchanged since January 2025, which is the problem.

There are five critical factors you need in order to get an invitation to the AI game:

- High-end GPUs, and lots of them

- Cheap energy

- High-quality data

- A favorable regulatory environment

- Talent

You can probably get away with 4 out of 5, or even 3 out of 5 if they are the right ones, but Germany would need 5 miracles; the same holds for most of Europe.

High-end GPUs. Germany’s position in the GPU arms race is behind by at least one order of magnitude, more realistically two to three, and the gap is widening. The current flagship, JUPITER at Jülich with its roughly 24k superchips, is celebrated as a continental achievement, and within the scientific computing world it is one. But the unit of account at the frontier has changed: xAI’s Memphis site, which I cited at 100k GPUs when starting this draft (and which was already five times the German flagship), has since doubled and been superseded by a successor site marketed in gigawatts; Stargate is a $500B program; the US hyperscalers collectively spend on the order of half a trillion dollars per year. Against that, Europe’s gigafactory initiative earmarks ~€20B for five sites, to be energized at some future date, pending procurement. Some might argue DeepSeek proves you do not need frontier-scale GPUs. Partially true, and worth taking seriously, but note what DeepSeek actually had: exceptional engineering talent and still-substantial compute (their V3 training run alone consumed 2.788 million GPU hours; and the famous “$5.6M” figure prices a single pretraining run, not the program around it). “GPU-poor” by US standards is still GPU-rich by German ones.

And note the access regime itself, because it is its own lesson. Outside the US, frontier GPUs come in exactly two flavors: nerfed or unavailable. China gets the nerfed flavor, deliberately degraded export models (H800s, H20s, whatever the deal of the season permits), and answered with smuggling, ruthless efficiency engineering, and a domestic accelerator stack (Huawei’s Ascend line and friends) that improves every quarter. China has a solution. Europe gets the other flavor: nothing is formally banned, you are simply not getting allocation. NVIDIA’s production is pre-sold years ahead to US hyperscalers, whatever reaches the market is rationed, and when Washington briefly formalized the hierarchy in the January 2025 “AI diffusion framework”, several EU member states (Poland and Portugal among them) woke up in Tier 2 with hard GPU quotas, to Brussels’ considerable fury, before the rule was rescinded in favor of deal-by-deal diplomacy. The reality remained the same though: GPU access is a privilege administered elsewhere. China’s answer is to build its own. Europe’s answer is a working group.

Cheap energy. Germany’s industrial electricity prices are among the highest of any major economy; for data centers the comparison is brutal (approximate, large industrial users, 2024/25; cf. IEA data):

| Country | ~USD/kWh (industrial) |

|---|---|

| Germany | 0.19 |

| France | 0.13 |

| United States | 0.08 |

| China | 0.08 |

| Norway | 0.06 |

And price is only half of it; the other half is buildout velocity. AI compute is, physically, an energy-conversion industry: whoever can connect gigawatts fastest wins. China connects a Germany’s worth of capacity per year; the US fast-tracks gas turbines and restarts nuclear plants next to data centers; Germany debates. So that’s a no, twice.

High-quality data. Germany faces structural barriers to accessing and using data at AI scale. GDPR, whatever its merits for individual privacy, created a data-scarce environment: explicit-consent regimes, retention and transfer restrictions, and compliance overhead that discourages exactly the kind of large-scale data aggregation that modern AI training requires. Cultural attitudes amplify the law: the population is unusually privacy-anxious, participation in data-sharing initiatives is low, and every digitization project ships with a built-in opposition committee. The result is a data ecosystem that is limited in scope, fragmented by design, and fundamentally misaligned with how AI systems are built. Meanwhile, the clinical, industrial, and administrative data that Europe does uniquely have sits in silos that even European researchers cannot use.

Favorable regulatory environment. Germany is known for a strong regulatory environment, just not the right one. The instinct is to regulate the risks of a technology before having the technology. The AI Act is the monument to this instinct: years of negotiation, a compliance industry spun up before a single European frontier model existed, and then, within fifteen months of entry into force, a Commission “omnibus” to delay and dilute it because reality refused to cooperate. The damage of such regulation is not even the direct compliance cost; it is the uncertainty tax and the signal. Founders price in that the rules can change twice before their Series B; many simply incorporate elsewhere. Regulation is drying out innovation, turning what could be a thriving tech ecosystem into a compliance landscape that only incumbents can afford to navigate.

Talent. The one factor where Europe genuinely competes, which makes the outcome more damning. Germany still produces excellent researchers and engineers (the education system’s last compounding asset), but it produces them for export. The brightest go where the compute, capital, and ambition are: historically the US, increasingly also Chinese labs. Student numbers in STEM are declining, the demographic pipeline is shrinking (more below), immigration processes remain a bureaucratic obstacle course, and the domestic ecosystem offers no gravitational pull: no critical mass of frontier work, no scale-ups, thin early-stage funding, and exit environments that make ambitious founders leave before they start. Funding, where it exists, is administered in homeopathic doses: tens of millions, spread across dozens of recipients, announced as strategy. The canonical example: OpenEuroLLM, Europe’s flagship answer to the DeepSeek moment, announced the very same week: €52 million, spread across a consortium of twenty research institutions, companies, and computing centers, complete with work packages, deliverables, and reporting obligations. That is roughly €2.6 million per partner before coordination overhead, deployed against labs whose weekly electricity bills run higher. A single US lab raises more in a week, for one idea, than such programs disburse in a year across a continent.

And on top of all of it sits culture. There is no nice of saying this: Germany does not currently have a culture of building. Economic growth itself has become suspect (“do we even want this?” is a serious question in serious newspapers), risk-taking is socially penalized, failure is disqualifying, and the comfortable default is to be an NPC in someone else’s game: consume the platforms, rent the models, regulate the externalities, and call the resulting role “digital sovereignty”. NGMI, as the kids say. The kids, incidentally, have mostly stopped saying it here; they said it from Palo Alto, Zurich, or Shenzhen.

What remains: niches, on shrinking product maps

So what is the realistic European AI play? Niches. And to be clear, some of them are excellent: DeepL built a world-class translation business in Cologne; Helsing became one of Europe’s most valuable startups doing defense AI; Black Forest Labs in Freiburg trains some of the best image models in the world; Mistral holds the credible-open-European-model franchise. Europe will get vertical wins in industrial AI, pharma, legal tech, defense, embedded systems. These are real companies with real revenue, and I am happy they exist.

But notice three things. First, niches live downstream of somebody else’s frontier. They fine-tune, distill, and deploy on chips, models, and clouds owned elsewhere; they are tenants, and tenants do not set the rent. Second, the niche outcome is the good scenario, and it also follows the pattern from above: great research upstream, disaster downstream. Another canonical example in plain sight. Latent diffusion, the technique underneath the entire image-generation industry, was invented in the CompVis group at Heidelberg/LMU Munich; the platform value was captured by Stability, Midjourney, and OpenAI, and only years later did some of the original authors found Black Forest Labs to claw a piece back. Same story one generation earlier: the LSTM was invented in Munich in the 1990s and powered Google’s speech and translation stack for a decade. Europe invents; others compound. The rock star plays; the audience, and the box office, are elsewhere.

Third, and this should worry even the comfortable: while Europe debates catching up, the products are quietly leaving. Apple is shipping its new Siri AI everywhere except the EU, with Cupertino and Brussels blaming each other for the delay. Google launched AI Edge Eloquent, a free on-device dictation app, in the US and most of the world, but not in the EEA; a fully offline app, so much for a privacy argument going berserk. Meta withheld its multimodal models from the EU back in 2024, and that was a precedent, not an exception. The sequel made it explicit: Llama 4’s license excludes anyone domiciled in the EU from its multimodal models outright, region-locking written directly into an “open” license. Apple Intelligence itself reached EU iPhones half a year late. OpenAI shipped (the now discontinued) Sora everywhere except Europe. None of this is a dramatic market exit: it is simply a region toggle in a release checklist, set to “skip” because expected compliance pain exceeds expected revenue; no f*#!s are given, and none are taken. And that is what makes this very dangerous. Each individual feature is dispensable, “not so important”, etc but the sum is a continent drifting product generations behind: nerfed, late, or never… as a way of life. And that capability gap compounds, so that a 5-year gap turns quickly into a 10-year gap and so on…

The four horsemen (this time they hit twice)

Underneath the policy failures sits something slower, worse, and much more fundamental. Four factors that shape a lot of what is to come as third-order or fourth-order effects. I call them the four horsemen, with effects through the individual (micro) and through the continent (macro).

1. Demography.

Micro: people vote with the most consequential ballot there is, by not having children. In the 2019 post I mused, half-jokingly, that “one might contemplate whether populations in several developed countries are shrinking in early anticipation of the times ahead.” It reads less like a joke now. Unfortunately.

Macro: inverted population pyramids, exploding old-age dependency ratios, and a shrinking workforce that must fund an expanding welfare state. More on this in the next section.

2. Attention.

Micro: the TikTok-formatted mind. Average sustained attention is collapsing into sub-minute fragments; long-form reading, the entry ticket to every hard skill, is in free fall among the young. If you have read this far, congratulations, you are statistically remarkable.

Macro: institutional attention collapsed to the election cycle and the news cycle. Compute buildouts, grids, and research ecosystems are decade-scale commitments; a system that re-litigates its energy policy every legislative period cannot make decade-scale commitments. A continent with a fried attention span gets exactly the infrastructure it can concentrate on: none.

3. Skill.

Micro: outsourcing thinking before having learned to think. Used well, AI is the greatest skill-amplifier ever built; used as a crutch from day one, it produces graduates with credentials and without capabilities, and early cognitive-offloading studies are not reassuring. (Jana wrote about the schools’ side of this here and see also the article The Great Cognitive Slowdown: Are We Getting Dumber?)

Macro: this is where the rock star without an audience lives. Europe still produces world-class researchers, rock stars by any technical measure, but there is no ecosystem around them: no labs at scale to join, no capital to build with, no industrial base that absorbs what they know; they perform, brilliantly, to an empty room, until they leave for a full one. And one generation further out it gets darker: an audience that no longer understands the performance. A next generation trained on fragments, with skills outsourced, lacks the depth to appreciate, use, or leverage the expertise of the generation before it. The transmission of competence (master to student, senior to junior) is broken not because the masters disappeared, but because the apprenticeship did.

4. Hyper-individualism.

Micro: the optimization of the self as the only remaining project; identity over contribution, wellness over works. A mindset of scarcity as modus operandi. And understandably so: in many respects this is the only rational answer to the current state of affairs.

Macro: it aggregates into a politics of refusal. Degrowth as a moral position, NIMBY as a default, and the quiet exits. People voting with their feet, with companies now having an easy, even fashionable, excuse to relocate to the US, and the current US administration is actively rolling out the red carpet. People voting with their money: European savings finance, with impressive reliability, everyone else’s buildouts. After all, who would want to put their money into Europe? NIMBY in the morning, and US equities in the afternoon when US markets open, to get at least some piece of the pie. Each individual decision is perfectly rational, as a whole though Europe is shorting itself.

And there is a somewhat degenerate coupling: AI amplifies horsemen two and three (it is the attention economy’s strongest drug and the skill-crutch par excellence) while being the only realistic antidote to horseman one:

AI against the demographic cliff

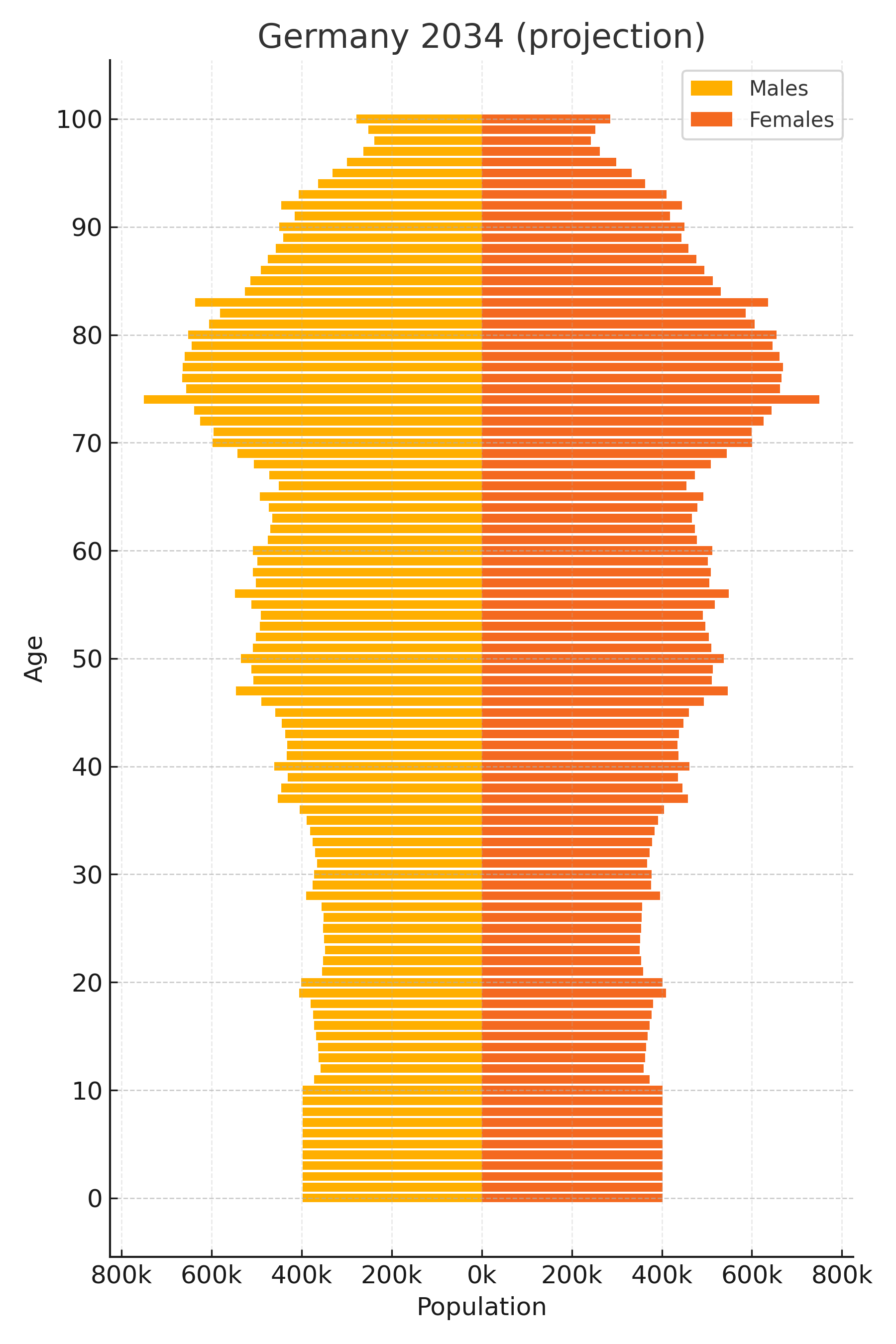

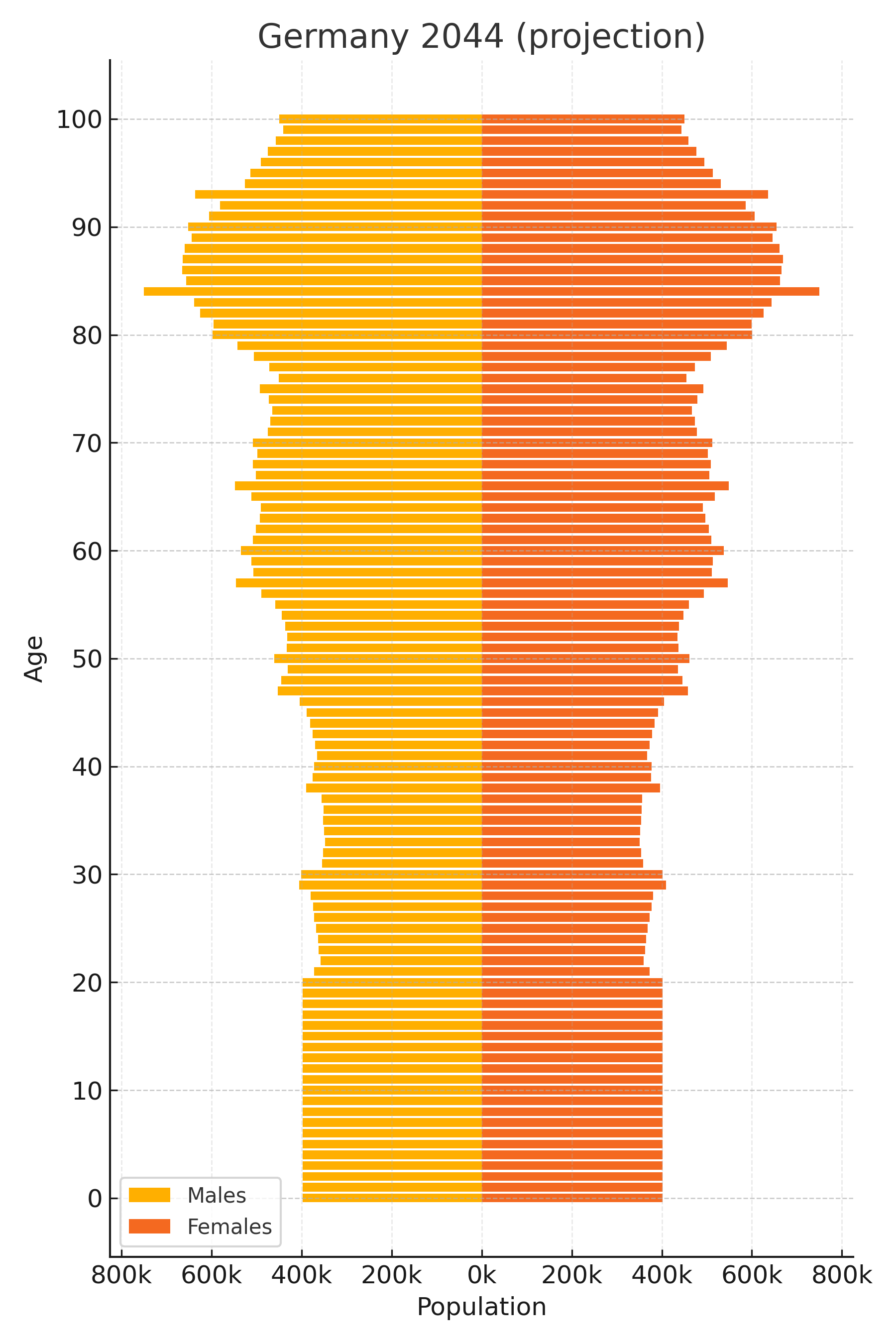

Here is Germany’s population structure, today and projected:

Figure 2: Germany’s population pyramid, 2024, and projections for 2034 and 2044. The boomer bulge moves from “working and paying” to “retired and drawing”, and nothing refills from below. Very optimistic projection with steady (i.e., optimistic) roll-forward.

The math is unforgiving: the German labor force shrinks by millions over the next decade as the boomers retire, while the number of pensioners and care recipients grows. Output is workers times output-per-worker. If the first factor falls structurally, the second must rise structurally, or the welfare state, healthcare, pensions, and ultimately political stability go with it. There is no third option; productivity is not a nice-to-have here, it is the pillar everything rests on. Former German foreign minister and vice chancellor Joschka Fischer (Green Party, of all people) put it bluntly in this spring’s (May 2026) pension debate, after Chancellor Merz had been booed at the trade-union congress for suggesting reform:

Buhrufe ändern die Mathematik nicht. (“Booing does not change the math.”)

And this is where the usual framing (“AI replaces labor and that is a cost story”) misses the point. It is not about labor cost; it is about friction. A shrinking workforce does not primarily make labor expensive, it makes it unavailable: positions unfilled for a year, projects unstaffed, care undelivered, permits unprocessed. AI’s economic magic is the removal of friction, not just cost: no hiring lag, no scarcity in the relevant skill, scaling on demand, around the clock. Hybridization, the 2019 thesis, is exactly the mechanism by which 70-year-olds’ pensions get paid by 40-year-olds operating at 3x: the AI handles the basics, the scarce human handles the rest. Japan understood this years ago and put robots (with mixed success) in care homes without a culture war. China, facing its own demographic cliff one decade behind ours, is betting on robots and AI at national scale, explicitly. The US solves it the old way, by importing and welcoming(!!!) people, including Europeans.

This is actually the bitterest irony of this whole story: the one bloc that needs the zeroth world the most is the one regulating and fighting it the hardest. Europe is demographically doomed to need a productivity miracle and culturally committed to preventing one. The 2019 post asked whether AI could create a zeroth world. The 2026 question is only who lives in it as it is being built either way.

Seven predictions for the next seven years

The 2019 post earned its update by making claims that could fail. Same rules again: seven predictions for 2033.

- No European frontier lab. By 2033, no EU-headquartered lab operates within an order of magnitude of frontier training compute. Mistral ends up acquired, consolidated into sovereign-cloud contracts, or excellent-but-niche.

- Feature lag stops being news. Flagship AI products launching in the EU six to twenty-four months late, feature-reduced, or never becomes standard practice; at least one defining consumer AI product of the early 2030s simply never ships in the EEA, and nobody is surprised.

- The gap reaches the statistics. US labor-productivity growth exceeds the euro area’s by a full percentage point or more on average over the period, and the transatlantic GDP-per-capita gap is wider in 2033 than today; the first unambiguous zeroth-world signatures show up in US sectoral data (software, professional services, parts of admin-heavy healthcare) around 2030.

- Europe’s AI-security shock. Before 2033, a major European infrastructure incident (a utility, a hospital group, a government system) is traced to a vulnerability class that Glasswing-tier organizations had already found and fixed on their own stacks. The response is emergency procurement from a US lab: sovereignty by invoice.

- China cashes the deployment dividend. China leads robot density and lights-out manufacturing by a comfortable margin, its open-weight stack becomes the default AI infrastructure of the Global South, and it becomes the first large economy to visibly offset a shrinking workforce with AI-plus-robotics in official statistics.

- Germany adopts AI through the back door. The care, administration, and SME-succession crunch forces mass AI adoption around 2029-2031, on imported stacks, faster than any digitization program ever managed, and without a single strategy paper being implemented as written.

- Gigafactory theater. EU AI gigafactories get inaugurated, with speeches and ribbons; by 2033 not one of them has hosted a frontier-scale training run, and the EU’s total public AI compute remains smaller than a single US hyperscaler’s annual addition.

If at least four of these turn out wrong, Europe will have surprised me in the best possible way, and nobody will be happier to write that scorecard.

Some final thoughts

I ended the 2019 post by writing that “in order to enable sustainable progress we need to not just be aware but prepare and actively shape the use of these new technologies.” I stand by the sentence, more than ever, with one amendment learned the hard way: shaping requires being at the table.

The zeroth world is no longer a thought experiment; the gap between it and the first world is opening in real time, in real numbers, in real locations, in real capabilities, in Memphis and Abilene and Shanghai. Seven years ago I asked what that gap would look like. The sobering 2026 answer is that Germany (and Europe) has decided to be a “Reallabor” (real-world laboratory), finding it out empirically in real-time… from the other side.

GERMAN TRANSLATION - AI-GENERATED, ZERO TOUCH-UPS

If you want to understand why the translation is worse than the English original, read “The hidden cost of tokenization”

Die Nullte Welt: ein Update nach sieben Jahren

TL;DR: Vor sieben Jahren habe ich argumentiert, dass KI eine nullte Welt ermöglichen könnte: Volkswirtschaften, die mit einem Vielfachen der Produktivität der Ersten Welt operieren, so wie die Erste Welt mit einem Vielfachen der Dritten operiert. Das Update: Die Technologie kam schneller, als ich erwartet hatte, die Produktivitätsgewinne sind real, aber ungleich verteilt, und die nullte Welt wird gerade gebaut, in den USA und in China. Europa ist bestens auf Kurs, von der Seitenlinie aus zuzuschauen, was besonders bitter ist, weil Europa sie demografisch nötiger hat als irgendwer sonst. Die neueste Wendung: Cyber-Abwehrfähigkeiten auf Frontier-Niveau werden jetzt auf Einladung vergeben, und Europa steht überwiegend nicht auf der Liste.

In meinem früheren Beitrag über die Nullte Welt habe ich die Auswirkungen künstlicher Intelligenz auf Gesellschaft und Wirtschaft diskutiert, mit Betonung auf den bereits vorhandenen und latenten Fähigkeiten statt auf spekulativen Zukunftsszenarien. Ich definierte KI als Systeme, die Informationen sammeln, lernen, entscheiden und autonom handeln, ähnlich der OODA-Schleife. Ich betonte die Notwendigkeit der Hybridisierung, bei der sich KI-Systeme mit Menschen zusammentun, um die Produktivität zu steigern und Abläufe zu skalieren. Beispiele waren autonomes Fahren, Callcenter und Portfoliomanagement. Außerdem ging es um das Potenzial von KI, eine „Nullte Welt“ mit beispiellosem Wirtschaftsoutput und Produktivitätsniveau zu schaffen; im Kern: Die nullte Welt verhält sich zur Ersten Welt, wie sich die Erste Welt beim Wirtschaftsoutput zur Dritten Welt verhält. Und ich habe, zumindest in Ansätzen, die Risiken von Jobverdrängung und Machtkonzentration diskutiert.

Das war vor sieben Jahren, geschrieben, als ich noch in den USA lebte, vor meinem Umzug nach Europa (genauer: Deutschland). Seitdem ist viel passiert, und das hier ist das Update. Volle Transparenz: Ich habe mit dem Update am 28. Januar 2025 begonnen (eigentlich als Sechs-Jahres-Update gedacht), in der Woche, in der DeepSeek R1 erschien. Dann lag es fast anderthalb Jahre im Entwurfsordner, während alles darin wahrer wurde.

Die Kulisse, vor der dieser Beitrag nun endlich erscheint, ist zu offensichtlich, um sie zu ignorieren: Heute, am 12. Juni 2026, geht SpaceX an die Börse, nachdem das Unternehmen 75 Milliarden Dollar eingesammelt hat, bei einer Bewertung von rund 1,8 Billionen Dollar, der größte Börsengang der Geschichte und etwa das Zweieinhalbfache des alten Rekords von Saudi Aramco; Anthropic und OpenAI haben ihre Börsenanträge eingereicht, innerhalb derselben zwei Wochen. Damit ist die nullte Welt jetzt eine handelbare Anlageklasse.

ANMERKUNG. Das Offensichtliche oder das wahrscheinlichste Ergebnis zu benennen ist keine Befürwortung.

Was der 2019er-Beitrag richtig sah (und was nicht)

Bevor ich neue Vorhersagen für die Zukunft mache, rechnen wir zuerst meine alten von 2019 ab.

Was saß:

- Hybridisierung war der richtige Call. Die These von 2019 war: Wir brauchen keine volle Autonomie, sondern einen Menschen im Gespann mit einer KI, die „90 % der Routine mit menschlichem Override“ erledigt. Das ist, fast wörtlich, das Deployment-Muster von 2023–2026: Copilots, Assistenten, Agenten mit Eskalation. Klarnas Assistent übernahm im ersten Monat zwei Drittel aller Kundenservice-Chats, die Arbeitslast mehrerer hundert Servicemitarbeiter. Das am besten untersuchte Callcenter-Deployment zeigte rund 14 % durchschnittlichen Produktivitätsgewinn, rund 34 % bei Anfängern. Callcenter waren buchstäblich das erste Beispiel auf meiner 2019er-Liste.

- Das Leitstellen-Modell fürs Fahren. 2019 skizzierte ich zwei Use Cases: Fernoperatoren, die mehrere Fahrzeuge überwachen, und Hub-zu-Hub-Autobahnautonomie für Lkw. Waymo fährt heute 500.000 bezahlte Robotaxi-Fahrten pro Woche in zehn US-Städten (mit dem erklärten Ziel von einer Million pro Woche bis Ende 2026), gestützt auf genau die Art von Remote-Flottenassistenz, die damals beschrieben wurde. Aurora startete 2025 fahrerlose Frachtfahrten zwischen Dallas und Houston, Hub-zu-Hub, exakt wie skizziert. Und meine Lieblingsfußnote: Teledriving, die reinste Form der Leitstellen-Idee, wird kommerziell von Vay angeboten… einem in Berlin gegründeten Unternehmen, das in Las Vegas operiert. Den merken wir uns für später.

- „In ein paar Jahren werdet ihr so einen Bot im App Store herunterladen.“ ChatGPT erschien im November 2022, dreieinhalb Jahre nach diesem Satz, und wurde die am schnellsten adoptierte Consumer-Anwendung der Geschichte. Die Schwester-Vorhersage, dass wir den Bau solcher Systeme bald Ende-zu-Ende als studentisches Abschlussprojekt an Universitäten lehren würden, heißt heute einfach: Curriculum.

- Machtkonzentration. Der 2019er-Beitrag spekulierte, dass „die nächste Größenkategorie von KI-Unternehmen definiert wird, mit einer wahnwitzigen Konzentration von Ressourcen, Reichtum und Macht, gegen die die heutige Konzentration im Valley verblasst“. NVIDIA wurde das erste Vier-Billionen-Dollar-Unternehmen; eine Handvoll US-Firmen gibt inzwischen in der Größenordnung von einer halben Billion Dollar pro Jahr für KI-Infrastruktur aus; die Spitze des S&P 500 ist, funktional betrachtet, ein KI-Index. Und seit dieser Woche hat die „nächste Größenkategorie“ Ticker: SpaceXs Rekord-Listing macht das Unternehmen vom ersten Tag an zu einem der größten Amerikas, mit OpenAI und Anthropic direkt dahinter, grob vier Billionen Dollar Nullte-Welt-Equity auf dem Weg an die öffentlichen Märkte, auf einmal. Diesen Punkt verbuche ich für mich.

- Der Compute-Trend. Die „Verdopplung alle 3,5 Monate“ beim Trainings-Compute konnte offensichtlich nicht in genau diesem Tempo weitergehen (jede Exponentialfunktion ist eine Sigmoide), aber der Kernpunkt hielt: dass wir schneller unterwegs waren als in jedem früheren Technologiezyklus. Der Trainings-Compute für Frontier-Modelle wuchs weiter um Vielfache pro Jahr, finanziert durch die Capex-Zahlen von oben.

Was daneben lag:

- Der Mechanismus. Ich schaute auf Reinforcement Learning und Self-Play (AlphaStar et al.). Der eigentliche Durchbruch kam aus selbstüberwachtem Lernen auf Text, in großem Maßstab. Die Form der Vorhersage (Fähigkeiten durch Compute-Skalierung, kein fundamentales Hindernis) stimmte; der Mechanismus nicht. Ich verbuche das als Glück an der Stelle, die zählt, und als Irrtum an der Stelle, die nicht zählt.

- Zeitpläne für die physische Welt. Das Fahren dauerte länger, als die Extrapolation der Disengagement-Raten nahelegte (kam aber). Robo-Advisors blieben mittelmäßig. Atome bleiben härter als Bits.

- Die Aggregatzahlen (bislang). Man sieht die nullte Welt noch immer nicht in den BIP-Statistiken. Produktivitätsstatistiken bewegen sich langsam, Diffusion ist klumpig, und wir sind früh dran. Das ist das klassische Solow-Problem: „Computer überall, außer in den Produktivitätsstatistiken.“ Was man aber bereits sehen kann, ist die Divergenz zwischen Blöcken, und genau die ist das eigentliche Thema dieses Updates.

Agenten: die OODA-Schleife par excellence

Wer die 2019er-Definition eines KI-Systems heute wieder liest, (1) wahrnehmen, (2) lernen, (3) entscheiden, (4) handeln, mit einem Maß an Autonomie, kann sich ein Lächeln kaum verkneifen: Das ist schlicht die Beschreibung eines Agenten des Jahres 2026. Tool Use, Computer Use, Coding-Agenten, Deep-Research-Agenten: die OODA-Schleife, kommerziell und in großem Maßstab. Was eine aus der Militärdoktrin entliehene Abstraktion war, ist jetzt eine Produktkategorie.

Und die Produktivitätsgewinne sind real, wenn auch ungleich verteilt. Ich werde die riesige Studienlage hier nicht referieren, nur zwei Kalibrierungspunkte: Anfängerlastige, klar umrissene Arbeit zeigt große Gewinne (die Callcenter-Zahlen oben), während METRs Studie von 2025 fand, dass erfahrene Open-Source-Entwickler mit KI-Tools auf ihren eigenen, vertrauten Codebasen tatsächlich langsamer waren, während sie sich schneller glaubten. Beide Ergebnisse stimmen; die Verteilung der Gewinne ist der entscheidende Punkt. Meine eigene Erfahrung, siehe den Beitrag The Agentic Researcher, ist, dass mit Verification-first-Workflows die Gewinne in der Forschungsarbeit sehr substanziell sind; und der Ausgewogenheit halber: nicht jede Entdeckung braucht ein LLM.

Eine der Kernhypothesen von 2019 war der Automate-and-Elevate-Zyklus: die Routine automatisieren, eine Ebene höher arbeiten, wiederholen. Das ist jetzt real, mit passend zugeschnittenen und passend betoolten Agenten. Der Individual Contributor des Jahres 2026 verhält sich zunehmend wie ein Manager von Prozessen, die zufällig in silico laufen; im Grunde ein Solo-Unternehmer. Das war der Mechanismus, über den ich ein 10x im Output pro Person für plausibel erklärte. Ich sehe keinen Grund, diese Behauptung zurückzunehmen, eher die Frage, wo es passieren wird und ob es sich aufzinst. Womit wir beim eigentlichen Update wären.

Das Rennen läuft jetzt zwischen Blöcken: USA, China, Europa

2019 dachte ich die nullte Welt in Ländern, die sich beim BIP pro Erwerbstätigem absetzen. 2026 ist die bessere Auflösung die in Blöcken, denn die Inputs, auf die es ankommt, liegen auf Block-Ebene: Compute, Energie, Daten, Regulierung, Kapital, Talent.

| Faktor | USA | China | Europa |

|---|---|---|---|

| Frontier-Compute | ✓✓ | ~ (beschränkt, kompensierend, ändert sich aber schnell) | ✗ |

| Energie (Preis & Ausbau) | ~ (billig, netzlimitiert) | ✓✓ | ✗ |

| Daten | ✓ | ✓✓ | ✗ (per Design) |

| Regulierung (für Builder) | ✓ | ✓ (pragmatisch) | ✗ |

| Kapital | ✓✓ | ✓ | ✗ (vorhanden, risikoscheu) |

| Talent | ✓✓ (importiert) | ✓✓ (Masse) | ✓ (exportiert) |

Die USA spielen das geschlossene Frontier-Spiel: eine Handvoll Labore, im Wesentlichen unbegrenztes Kapital und Compute-Ausbauten, die die Kategorie „Rechenzentrum“ hinter sich gelassen haben und zum „Industrieprogramm“ geworden sind. Stargate wurde mit 500 Milliarden Dollar angekündigt, in genau der Woche, in der ich diesen Entwurf begann; xAIs erster Memphis-Cluster, den ich ursprünglich mit 100.000 GPUs als unerhörte Zahl zitierte, hat die 200.000 überschritten, und der Nachfolgestandort wird in Gigawatt vermarktet statt in Chip-Zahlen. Die bindende Restriktion in den USA ist nicht mehr Geld oder Chips; es sind Strom und Netzanschlüsse.

China spielt das offene und das Deployment-Spiel, und der DeepSeek-Moment war kein Einzelfall. Qwen, Kimi, GLM, MiniMax: Die meistgenutzten Open-Weight-Modelle der Welt sind heute, mit komfortablem Abstand, chinesisch, was bedeutet, dass das Default-Substrat für alle außerhalb der Frontier-Labore zunehmend chinesisch ist. Compute ist der limitierende Input (Exportkontrollen wirken, teilweise), aber die Antwort darauf waren Effizienz-Engineering plus ein heimischer Beschleuniger-Stack, der schnell reift. Und der Vorstoß geht den ganzen Stack hinunter: Reuters hat ein staatlich orchestriertes „Manhattan-Projekt“ um Huawei dokumentiert, das die Chip-Werkzeugkette selbst replizieren soll, bis hin zu der einen Maschine, von der alle dachten, sie sei nicht replizierbar: ASMLs EUV-Lithografie. Heimische EUV-Prototypen sind Berichten zufolge im Test, mit KI-Chip-Produktion angepeilt für 2028 (Insider sagen 2030; Analysten sagten früher: ein Jahrzehnt). Man darf die Prahlerei gern diskontieren, seriöse Einschätzungen tun das, aber die Richtung ist eindeutig: Der Engpass wird ingenieurtechnisch umgangen. Europa sollte das einen Moment sacken lassen, denn ASML in Veldhoven ist das einzige echte KI-relevante Druckmittel des Kontinents, und der Countdown, dieses Druckmittel zu beenden, läuft. Bei Energie gibt es keinen Wettbewerb: China hat letztes Jahr mehr Erzeugungskapazität zugebaut, als Deutschland insgesamt betreibt, hat im ersten Halbjahr 2025 mehr als doppelt so viel Solar installiert wie der Rest der Welt zusammen, und seine kumulierte Solarflotte überschritt 2025 die Terawatt-Marke, vieles davon in Wüsten-Megabasen wie der „Großen Solarmauer“ von Kubuqi, der Art Infrastruktur, der man vom Weltall aus beim Wachsen zusehen kann. Und entscheidend: China dominiert die Schicht, in der Nullte-Welt-Produktivität die physische Ökonomie berührt: Industrieroboter (rund die Hälfte der globalen Installationen), E-Autos, Batterien, elektrifizierte Fertigung. Wenn die USA das Hirn besitzen, besitzt China den Stoffwechsel.

Europa spielt das Kunden-Spiel und nennt es das Werte-Spiel. Der EU AI Act trat 2024 in Kraft; im November 2025 schlug die Kommission per Digital Omnibus bereits vor, genau die Regeln zu verschieben und aufzuweichen, deren Verabschiedung sie gerade noch gefeiert hatte, nach der vorhersehbaren Erkenntnis, dass sie nicht umsetzbar waren. Erst regulieren, dann zurückrudern, niemals bauen. Beim Compute ist Europas stolzeste Maschine, JUPITER in Jülich (Europas erstes Exascale-System, rund 24.000 Superchips), ein feines wissenschaftliches Instrument und ein Rundungsfehler gegen einen einzelnen US-Standort. Die Schlagzeilen-Antwort, InvestAI mit 200 Milliarden Euro und „KI-Gigafabriken“, bleibt, Stand heute, im Wesentlichen eine Anlageklasse aus Pressemitteilungen. Der Draghi-Bericht hat im September 2024 alles gesagt, was zu sagen war, in Amtsprosa, mit Zahlen; bemerkenswert wenig ist seitdem passiert. Mistral existiert und ist wirklich gut, was es zur Ausnahme macht, die die Regel bestätigt; Aleph Alpha, die deutsche Frontier-Hoffnung, stieg 2024 aus dem Frontier-Rennen aus.

Der absorbierende Zustand scheint offensichtlich: Die nullte Welt wird kein Country Club, bei dem man einen Aufnahmeantrag stellen kann. Es läuft auf zwei Ökosysteme hinaus, eine US-geführte geschlossene Frontier und einen chinesisch geführten Open/Deployment-Stack, plus Kunden. Europa entscheidet sich gerade, mit großer prozeduraler Sorgfalt und der unbeirrbaren Exaktheit der Bürokratie, Kunde zu sein.

Und das Kundendasein gibt es, wie sich herausstellt, jetzt auch in Stufen.

Die Glasswing-Asymmetrie: Sicherheit auf Einladung

Im April 2026 kündigte Anthropic Project Glasswing an, eine Initiative zur „Absicherung der kritischsten Software der Welt“, gebaut um frühen Zugang zu seinem neuesten Frontier-Modell, Claude Mythos Preview. Die definierende Fähigkeit des Modells ist das Finden und Beheben von Software-Schwachstellen in Maschinengeschwindigkeit; es hatte zur Ankündigung „bereits Tausende Zero-Day-Schwachstellen in kritischer Infrastruktur identifiziert“, und binnen Wochen meldeten die Startpartner über 10.000 Schwachstellen hoher oder kritischer Schwere in ihren Codebasen. Man halte hier kurz inne: Die Find-and-Fix-Schleife der Cybersicherheit läuft jetzt in KI-Geschwindigkeit, das Fenster von Schwachstelle zu Exploit schrumpft von Monaten auf Minuten, und dieselbe Fähigkeitsklasse wird ungefähr einen Open-Weight-Release-Zyklus später in den Händen von Angreifern sein. Die Verwundbarkeitsuhr hat für alle gleichzeitig zu ticken begonnen: Aber wer wird zuerst gehärtet?

Die elf benannten Startpartner: Amazon Web Services, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorganChase, die Linux Foundation, Microsoft, NVIDIA, Palo Alto Networks; nicht nur America first, sondern exklusiv. Die Erweiterung auf rund 150 weitere Organisationen in über fünfzehn Ländern wurde, in Anthropics eigenen Worten, „nach mehreren Wochen enger Zusammenarbeit“ mit Partnern, der Sicherheitsindustrie, Open-Source-Maintainern und der US-Regierung entschieden. Einzelne europäische Organisationen kommen rein (BT trat im Juni bei, in einer Erweiterungsrunde, nach Erfüllung von Anthropics Sicherheitsanforderungen), aber Einladung-als-Ausnahme ist hier der Punkt: Zugang zur defensiven Frontier ist diskretionär, widerruflich und läuft über San Francisco und Washington. Privilegierter Zugang ist Industriepolitik geworden, und Härtung ist (eine neue Schicht von) Exportkontrolle. Niemand hat Europa irgendetwas verboten, es ist nur ganz hinten in der Schlange gelandet.

Für die Nullte-Welt-Erzählung kommt damit eine zweite Dimension hinzu. Die erste Dimension war Produktivität; diese hier ist Verwundbarkeit. Die USA nutzen Frontier-KI, um systematisch zuerst den eigenen Stack zu härten: ihre Clouds, ihre Chips, ihre Banken, ihr Open-Source-Substrat. Europa läuft auf weiten Teilen derselben Software, also erbt es Patches flussabwärts, nach dem Zeitplan der Anbieter und gemäß deren Prioritäten. Aber Europas eigener Stack, die SAPs und Siemens-Steuerungen, die Versorger, die Krankenhaus-IT, die Behördensysteme, der Long Tail europäischen Codes aus fragmentierten Souveränitäts-Reflexreaktionen, der niemanden in Memphis interessiert, hat keinen Platz an diesem Tisch und keinen Zugang zu Frontier-Härtungsfähigkeiten. Kein Problem, machen wir eben unser eigenes Project Glasswing in Europa? Europa kann nicht einfach sein eigenes Glasswing fahren, denn ein Glasswing setzt ein Mythos voraus, und Europa hat kein Frontier-Modell, über dessen Zugang es einen solchen Härtungsvorsprung erzeugen könnte. Anders gesagt: Die Fähigkeitslücke ist zur Sicherheitslücke geworden, und dafür gibt es im Grunde keinen Fix.

Bemerkenswert ist auch, dass diese Episode erhellender ist als ein Jahrzehnt von Souveränitäts-Weißbüchern voller Hypothesen; die Komik dabei: Es wurde so viel geschrieben, und trotzdem hat diesen Fall niemand kommen sehen. Während Europa Jahre damit verbrachte, horizontale KI-Regulierung zu entwerfen, geschah die tatsächliche Allokation von Sicherheit im KI-Zeitalter, der wohl souveränitätsrelevantesten Ressource überhaupt, über eine Partnerliste, zusammengestellt von einem privaten amerikanischen Unternehmen in Abstimmung mit seiner Heimatregierung, binnen Wochen. So sieht Technikgestaltung aus, wenn man am Tisch sitzt. Und das ist die Definition davon, ein NPC zu sein (nicht einmal als Nachgedanke vorzukommen), wenn man es nicht tut.

Warum Europa im KI-Rennen nie aufholen wird

Ich nehme Deutschland als durchgehendes Beispiel, teils weil ich das System kenne (und hier lebe), teils weil Deutschland die größte Volkswirtschaft des Blocks und richtungsweisend repräsentativ ist; das Argument überträgt sich mit kleinen Anpassungen auf die meisten anderen Länder des Kontinents.

Zum Einstieg ein kurzer Zeitkapsel-Moment: Am 28. Januar 2025, als ich diesen Entwurf begann, hatte DeepSeek gerade seine offenen Modelle veröffentlicht (V3, R1, Janus-Pro) und chinesische Modelle damit auf Augenhöhe mit den besten des Westens gebracht, trainiert auf exportkontrollierten, kastrierten GPUs zu einem Bruchteil des üblichen Preispunkts. Es schickte die Börse auf Talfahrt („KI in den USA ist erledigt“), nur damit sie am nächsten Tag das meiste wieder aufholte („Moment mal, billigere KI heißt mehr Nutzer, und mehr Nutzer heißt mehr Geld“); dieselbe Geschichte wie bei den Dampfmaschinen. Jemand schickte mir in jener Woche ein Meme, das die Lage bis heute zusammenfasst:

Abbildung 1: Eine Zusammenfassung des Stands von KI in Deutschland und, allgemeiner, in Europa. Unverändert seit Januar 2025, was genau das Problem ist.

Es gibt fünf kritische Faktoren, die man braucht, um eine Einladung zum KI-Spiel zu bekommen:

- High-End-GPUs, und zwar viele

- Billige Energie

- Hochwertige Daten

- Ein günstiges regulatorisches Umfeld

- Talent

Mit 4 von 5 kommt man vermutlich durch, vielleicht sogar mit 3 von 5, wenn es die richtigen sind, aber Deutschland bräuchte 5 Wunder; dasselbe gilt für den Großteil Europas.

High-End-GPUs. Deutschlands Position im GPU-Wettrüsten liegt mindestens eine Größenordnung zurück, realistischer zwei bis drei, und die Lücke wächst. Das aktuelle Flaggschiff, JUPITER in Jülich mit seinen rund 24.000 Superchips, wird als kontinentale Errungenschaft gefeiert, und innerhalb des wissenschaftlichen Rechnens ist es eine. Aber die Maßeinheit an der Frontier hat sich geändert: xAIs Memphis-Standort, den ich zu Beginn dieses Entwurfs mit 100.000 GPUs zitierte (und der damals schon das Fünffache des deutschen Flaggschiffs war), hat sich seitdem verdoppelt und wurde von einem Nachfolgestandort abgelöst, der in Gigawatt vermarktet wird; Stargate ist ein 500-Milliarden-Dollar-Programm; die US-Hyperscaler geben zusammen in der Größenordnung von einer halben Billion Dollar pro Jahr aus. Dagegen reserviert Europas Gigafabrik-Initiative rund 20 Milliarden Euro für fünf Standorte, ans Netz zu gehen zu einem zukünftigen Datum, vorbehaltlich Vergabeverfahren. Manche wenden ein, DeepSeek beweise, dass man keine GPUs im Frontier-Maßstab braucht. Teilweise wahr, und ernst zu nehmen, aber man beachte, was DeepSeek tatsächlich hatte: außergewöhnliches Engineering-Talent und immer noch substanziellen Compute (allein ihr V3-Trainingslauf verbrauchte 2,788 Millionen GPU-Stunden; und die berühmten „5,6 Millionen Dollar“ bepreisen einen einzelnen Pretraining-Lauf, nicht das Programm drumherum). „GPU-arm“ nach US-Maßstäben ist nach deutschen immer noch GPU-reich.

Und man beachte das Zugangsregime selbst, denn es ist eine eigene Lektion. Außerhalb der USA gibt es Frontier-GPUs in genau zwei Geschmacksrichtungen: generft oder nicht verfügbar. China bekommt die generfte Sorte, absichtlich gedrosselte Exportmodelle (H800er, H20er, was der Deal der Saison gerade erlaubt), und antwortete mit Schmuggel, kompromisslosem Effizienz-Engineering und einem heimischen Beschleuniger-Stack (Huaweis Ascend-Linie und Verwandte), der jedes Quartal besser wird. China hat eine Lösung. Europa bekommt die andere Sorte: Nichts ist formal verboten, man bekommt nur schlicht keine Zuteilung. NVIDIAs Produktion ist auf Jahre an US-Hyperscaler vorverkauft, was den Markt erreicht, wird rationiert, und als Washington die Hierarchie im Januar 2025 mit dem „AI Diffusion Framework“ kurzzeitig formalisierte, wachten mehrere EU-Mitgliedstaaten (darunter Polen und Portugal) in Tier 2 mit harten GPU-Quoten auf, zu Brüssels erheblichem Zorn, bevor die Regel zugunsten von Deal-für-Deal-Diplomatie kassiert wurde. Die Realität blieb dieselbe: GPU-Zugang ist ein Privileg, das anderswo verwaltet wird. Chinas Antwort ist, eigene zu bauen. Europas Antwort ist eine Arbeitsgruppe.

Billige Energie. Deutschlands Industriestrompreise gehören zu den höchsten aller großen Volkswirtschaften; für Rechenzentren ist der Vergleich brutal (näherungsweise, große Industrieabnehmer, 2024/25; vgl. IEA-Daten):

| Land | ~USD/kWh (Industrie) |

|---|---|

| Deutschland | 0,19 |

| Frankreich | 0,13 |

| USA | 0,08 |

| China | 0,08 |

| Norwegen | 0,06 |

Und der Preis ist nur die Hälfte; die andere Hälfte ist Ausbaugeschwindigkeit. KI-Compute ist, physikalisch betrachtet, eine Energieumwandlungsindustrie: Wer am schnellsten Gigawatt anschließen kann, gewinnt. China schließt pro Jahr ein ganzes Deutschland an Kapazität an; die USA beschleunigen Gasturbinen und reaktivieren Kernkraftwerke neben Rechenzentren; Deutschland debattiert. Also: zweimal Nein.

Hochwertige Daten. Deutschland hat strukturelle Hürden beim Zugang zu und der Nutzung von Daten im KI-Maßstab. Die DSGVO, was immer ihre Verdienste für die individuelle Privatsphäre sind, hat ein datenarmes Umfeld geschaffen: Einwilligungsregimes, Speicher- und Übertragungsbeschränkungen und Compliance-Aufwand, der genau die Art großskaliger Datenaggregation entmutigt, die modernes KI-Training erfordert. Kulturelle Haltungen verstärken das Gesetz: Die Bevölkerung ist ungewöhnlich datenschutzängstlich, die Beteiligung an Daten-Initiativen niedrig, und jedes Digitalisierungsprojekt wird mit eingebautem Oppositionskomitee ausgeliefert. Das Ergebnis ist ein Datenökosystem, das in der Reichweite begrenzt, per Design fragmentiert und fundamental quer zu der Art liegt, wie KI-Systeme gebaut werden. Derweil liegen die klinischen, industriellen und administrativen Daten, die Europa tatsächlich einzigartig hat, in Silos, die nicht einmal europäische Forscher nutzen können.

Günstiges regulatorisches Umfeld. Deutschland ist bekannt für ein starkes regulatorisches Umfeld, nur eben nicht das richtige. Der Instinkt ist, die Risiken einer Technologie zu regulieren, bevor man die Technologie hat. Der AI Act ist das Denkmal dieses Instinkts: Jahre der Verhandlung, eine Compliance-Industrie hochgezogen, bevor ein einziges europäisches Frontier-Modell existierte, und dann, binnen fünfzehn Monaten nach Inkrafttreten, ein Kommissions-„Omnibus“ zum Verschieben und Verwässern, weil die Realität nicht kooperieren wollte. Der Schaden solcher Regulierung ist nicht einmal primär der direkte Compliance-Aufwand; es ist die Unsicherheitssteuer und das Signal. Gründer preisen ein, dass sich die Regeln vor ihrer Series B zweimal ändern können; viele inkorporieren einfach woanders. Regulierung trocknet die Innovation aus und verwandelt, was ein blühendes Tech-Ökosystem sein könnte, in eine Compliance-Landschaft, die sich nur Incumbents leisten können.

Talent. Der eine Faktor, bei dem Europa wirklich konkurrenzfähig ist, was das Ergebnis umso vernichtender macht. Deutschland bildet weiterhin exzellente Forscher und Ingenieure aus (der letzte Zinseszins-Aktivposten des Bildungssystems), aber es bildet sie für den Export aus. Die Besten gehen dorthin, wo Compute, Kapital und Ambition sind: historisch die USA, zunehmend auch chinesische Labore. Die Studierendenzahlen in MINT sinken, die demografische Pipeline schrumpft (mehr dazu unten), Einwanderungsprozesse bleiben ein bürokratischer Hindernislauf, und das heimische Ökosystem entwickelt keine Anziehungskraft: keine kritische Masse an Frontier-Arbeit, keine Scale-ups, dünne Frühphasenfinanzierung und Exit-Umgebungen, die ambitionierte Gründer gehen lassen, bevor sie anfangen. Förderung, wo es sie gibt, wird in homöopathischen Dosen verabreicht: zweistellige Millionenbeträge, verteilt über Dutzende Empfänger, verkündet als Strategie. Das kanonische Beispiel: OpenEuroLLM, Europas Flaggschiff-Antwort auf den DeepSeek-Moment, angekündigt in genau derselben Woche: 52 Millionen Euro, verteilt auf ein Konsortium von zwanzig Forschungseinrichtungen, Unternehmen und Rechenzentren, komplett mit Arbeitspaketen, Deliverables und Berichtspflichten. Das sind rund 2,6 Millionen Euro pro Partner vor Koordinations-Overhead, ins Feld geführt gegen Labore, deren wöchentliche Stromrechnungen höher liegen. Ein einzelnes US-Labor sammelt in einer Woche, für eine Idee, mehr ein, als solche Programme in einem Jahr über einen Kontinent ausschütten.

Und über allem sitzt Kultur. Es gibt keine nette Art, das zu sagen: Deutschland hat derzeit keine Kultur des Bauens. Wirtschaftswachstum selbst ist suspekt geworden („Wollen wir das überhaupt?“ ist eine ernsthafte Frage in ernsthaften Zeitungen), Risikobereitschaft wird sozial bestraft, Scheitern disqualifiziert, und der bequeme Default ist, NPC im Spiel von jemand anderem zu sein: die Plattformen konsumieren, die Modelle mieten, die Externalitäten regulieren und die resultierende Rolle „digitale Souveränität“ nennen. NGMI, wie die Kids sagen. Die Kids haben übrigens größtenteils aufgehört, es hier zu sagen; sie sagten es aus Palo Alto, Zürich oder Shenzhen.

Was bleibt: Nischen, auf schrumpfenden Produktkarten

Was ist also der realistische europäische KI-Play? Nischen. Und um fair zu sein, einige davon sind exzellent: DeepL hat in Köln ein Weltklasse-Übersetzungsgeschäft aufgebaut; Helsing wurde mit Verteidigungs-KI zu einem der wertvollsten Start-ups Europas; Black Forest Labs in Freiburg trainiert einige der besten Bildmodelle der Welt; Mistral hält die Franchise „glaubwürdiges offenes europäisches Modell“. Europa wird vertikale Erfolge bekommen, in Industrie-KI, Pharma, Legal Tech, Verteidigung, eingebetteten Systemen. Das sind echte Unternehmen mit echten Umsätzen, und ich bin froh, dass es sie gibt.

Aber man beachte drei Dinge. Erstens: Nischen leben flussabwärts von der Frontier eines anderen. Sie finetunen, destillieren und deployen auf Chips, Modellen und Clouds, die anderswo gehören; sie sind Mieter, und Mieter setzen nicht die Miete. Zweitens: Das Nischen-Ergebnis ist das gute Szenario, und auch es folgt dem Muster von oben: große Forschung flussaufwärts, Desaster flussabwärts. Noch ein kanonisches Beispiel in Sichtweite. Latent Diffusion, die Technik unter der gesamten Bildgenerierungsindustrie, wurde in der CompVis-Gruppe in Heidelberg/an der LMU München erfunden; den Plattformwert ernteten Stability, Midjourney und OpenAI, und erst Jahre später gründeten einige der ursprünglichen Autoren Black Forest Labs, um sich ein Stück zurückzuholen. Dieselbe Geschichte eine Generation früher: Das LSTM wurde in den 1990ern in München erfunden und trieb ein Jahrzehnt lang Googles Sprach- und Übersetzungsstack an. Europa erfindet; andere zinsen auf. Der Rockstar spielt; das Publikum, und die Abendkasse, sind woanders.

Drittens, und das sollte selbst die Bequemen beunruhigen: Während Europa übers Aufholen debattiert, verlassen die Produkte leise den Kontinent. Apple liefert sein neues Siri AI überallhin außer in die EU, während Cupertino und Brüssel sich gegenseitig die Schuld an der Verzögerung zuweisen. Google hat AI Edge Eloquent gestartet, eine kostenlose On-Device-Diktier-App, in den USA und fast überall sonst, aber nicht im EWR; eine vollständig offline laufende App, wohlgemerkt; so viel zum Amok laufenden Datenschutzargument. Meta hielt seine multimodalen Modelle 2024 von der EU zurück, und das war ein Präzedenzfall, keine Ausnahme. Die Fortsetzung machte es explizit: Llama 4s Lizenz schließt jeden mit Sitz in der EU von seinen multimodalen Modellen rundheraus aus, Region-Locking, direkt in eine „offene“ Lizenz geschrieben. Apple Intelligence selbst erreichte EU-iPhones mit einem halben Jahr Verspätung. OpenAI lieferte (das inzwischen eingestellte) Sora überallhin außer nach Europa. Nichts davon ist ein dramatischer Marktaustritt: Es ist schlicht ein Regionen-Schalter in einer Release-Checkliste, gesetzt auf „skip“, weil erwartete Compliance-Schmerzen den erwarteten Umsatz übersteigen; keine F*#!s werden gegeben, und keine genommen. Und genau das macht es so gefährlich. Jedes einzelne Feature ist verzichtbar, „nicht so wichtig“ etc., aber die Summe ist ein Kontinent, der Produktgenerationen zurückfällt: generft, verspätet oder gar nicht… als Lebensweise. Und diese Fähigkeitslücke zinst sich auf, sodass aus einer 5-Jahres-Lücke schnell eine 10-Jahres-Lücke wird und so weiter…

Die vier Reiter (diesmal treffen sie doppelt)

Unter den Politikversagen liegt etwas Langsameres, Schlimmeres und viel Fundamentaleres. Vier Faktoren, die als Effekte dritter und vierter Ordnung vieles von dem prägen, was kommt. Ich nenne sie die vier Reiter, mit Wirkung durch das Individuum (mikro) und durch den Kontinent (makro).

1. Demografie.

Mikro: Menschen stimmen mit dem folgenreichsten Stimmzettel ab, den es gibt, indem sie keine Kinder bekommen. Im 2019er-Beitrag sinnierte ich, halb im Scherz, dass „man darüber nachdenken könnte, ob die Bevölkerungen mehrerer entwickelter Länder in früher Vorwegnahme der kommenden Zeiten schrumpfen“. Es liest sich heute weniger wie ein Scherz. Leider.

Makro: invertierte Bevölkerungspyramiden, explodierende Altenquotienten und eine schrumpfende Erwerbsbevölkerung, die einen expandierenden Wohlfahrtsstaat finanzieren muss. Mehr dazu im nächsten Abschnitt.

2. Aufmerksamkeit.

Mikro: der TikTok-formatierte Geist. Die durchschnittliche Daueraufmerksamkeit kollabiert in Sub-Minuten-Fragmente; Langform-Lesen, das Eintrittsticket zu jeder anspruchsvollen Fähigkeit, ist bei den Jungen im freien Fall. Wer bis hierher gelesen hat: Glückwunsch, das ist statistisch bemerkenswert.

Makro: Institutionelle Aufmerksamkeit ist auf den Wahlzyklus und den Nachrichtenzyklus kollabiert. Compute-Ausbauten, Netze und Forschungsökosysteme sind Dekaden-Commitments; ein System, das seine Energiepolitik jede Legislaturperiode neu verhandelt, kann keine Dekaden-Commitments eingehen. Ein Kontinent mit frittierter Aufmerksamkeitsspanne bekommt genau die Infrastruktur, auf die er sich konzentrieren kann: keine.

3. Können.

Mikro: das Denken auslagern, bevor man denken gelernt hat. Gut eingesetzt ist KI der größte Fähigkeitsverstärker, der je gebaut wurde; als Krücke vom ersten Tag an produziert sie Absolventen mit Abschlüssen und ohne Fähigkeiten, und die frühen Studien zum Cognitive Offloading sind nicht beruhigend. (Jana hat über die Schulseite davon hier geschrieben; siehe auch den Artikel The Great Cognitive Slowdown: Are We Getting Dumber?)

Makro: Hier wohnt der Rockstar ohne Publikum. Europa produziert weiterhin Weltklasse-Forscher, Rockstars nach jedem fachlichen Maßstab, aber es gibt kein Ökosystem um sie herum: keine Labore im großen Maßstab zum Andocken, kein Kapital zum Bauen, keine industrielle Basis, die aufnimmt, was sie wissen; sie spielen, brillant, vor leerem Saal, bis sie in einen vollen wechseln. Und eine Generation weiter wird es dunkler: ein Publikum, das die Darbietung nicht mehr versteht. Eine nächste Generation, trainiert auf Fragmenten, mit ausgelagerten Fähigkeiten, hat nicht die Tiefe, die Expertise der Generation davor zu würdigen, zu nutzen, zu hebeln. Die Weitergabe von Kompetenz (Meister zu Schüler, Senior zu Junior) bricht nicht, weil die Meister verschwanden, sondern weil die Lehre verschwand.

4. Hyper-Individualismus.

Mikro: die Optimierung des Selbst als letztes verbliebenes Projekt; Identität über Beitrag, Wellness über Werk. Eine Knappheitsmentalität als Modus Operandi. Und verständlicherweise: In vieler Hinsicht ist das die einzig rationale Antwort auf den gegenwärtigen Zustand der Dinge.

Makro: Im Aggregat wird daraus eine Politik der Verweigerung. Degrowth als moralische Position, NIMBY als Default, und die leisen Abgänge. Menschen stimmen mit den Füßen ab, Unternehmen haben jetzt eine bequeme, geradezu modische Ausrede für den Umzug in die USA, und die aktuelle US-Regierung rollt aktiv den roten Teppich aus. Menschen stimmen mit ihrem Geld ab: Europäische Ersparnisse finanzieren, mit beeindruckender Zuverlässigkeit, die Ausbauten aller anderen. Wer würde sein Geld auch in Europa anlegen wollen? NIMBY am Vormittag, US-Aktien am Nachmittag, wenn die US-Märkte öffnen, um wenigstens ein Stück vom Kuchen abzubekommen. Jede Einzelentscheidung ist vollkommen rational, in Summe aber shortet Europa sich selbst.

Und es gibt eine etwas degenerierte Kopplung: KI verstärkt die Reiter zwei und drei (sie ist die stärkste Droge der Aufmerksamkeitsökonomie und die Fähigkeits-Krücke par excellence), während sie das einzige realistische Gegenmittel gegen Reiter eins ist:

KI gegen die demografische Klippe

Hier ist Deutschlands Bevölkerungsstruktur, heute und projiziert:

Abbildung 2: Deutschlands Bevölkerungspyramide 2024 und Projektionen für 2034 und 2044. Der Boomer-Bauch wandert von „arbeitet und zahlt ein“ zu „in Rente und bezieht“, und von unten füllt nichts nach. Sehr optimistische Projektion mit stetiger (d. h. optimistischer) Fortschreibung.

Die Mathematik ist unerbittlich: Die deutsche Erwerbsbevölkerung schrumpft im nächsten Jahrzehnt um Millionen, während die Boomer in Rente gehen und die Zahl der Rentner und Pflegebedürftigen wächst. Output ist Erwerbstätige mal Output pro Erwerbstätigem. Fällt der erste Faktor strukturell, muss der zweite strukturell steigen, oder Wohlfahrtsstaat, Gesundheitswesen, Renten und am Ende die politische Stabilität gehen mit. Eine dritte Option gibt es nicht; Produktivität ist hier kein Nice-to-have, sie ist der Pfeiler, auf dem alles ruht. Der frühere Außenminister und Vizekanzler Joschka Fischer (ausgerechnet ein Grüner) brachte es in der Rentendebatte dieses Frühjahrs (Mai 2026) unverblümt auf den Punkt, nachdem Kanzler Merz auf dem Gewerkschaftskongress für Reformvorschläge ausgebuht worden war:

Buhrufe ändern die Mathematik nicht.

Und genau hier geht der übliche Frame („KI ersetzt Arbeit, also ist das eine Kostengeschichte“) am Punkt vorbei. Es geht nicht um Arbeitskosten; es geht um Reibung. Eine schrumpfende Erwerbsbevölkerung macht Arbeit nicht primär teuer, sie macht sie unverfügbar: Stellen, die ein Jahr unbesetzt bleiben, Projekte ohne Besetzung, Pflege, die nicht geleistet wird, Genehmigungen, die nicht bearbeitet werden. Die ökonomische Magie der KI ist das Entfernen von Reibung, nicht nur von Kosten: kein Einstellungs-Lag, keine Knappheit bei der relevanten Fähigkeit, Skalierung auf Abruf, rund um die Uhr. Hybridisierung, die These von 2019, ist exakt der Mechanismus, über den die Renten der 70-Jährigen von 40-Jährigen bezahlt werden, die mit 3x operieren: Die KI übernimmt die Routine, der knappe Mensch den Rest. Japan hat das vor Jahren verstanden und Roboter (mit gemischtem Erfolg) in Pflegeheime gebracht, ohne Kulturkampf. China, dessen eigene demografische Klippe ein Jahrzehnt hinter unserer liegt, setzt explizit auf Roboter und KI im nationalen Maßstab. Die USA lösen es auf die alte Art, indem sie Menschen importieren und willkommen heißen(!!!), auch Europäer.

Das ist tatsächlich die bitterste Ironie dieser ganzen Geschichte: Der eine Block, der die nullte Welt am nötigsten hat, ist der, der sie am härtesten reguliert und bekämpft. Europa ist demografisch dazu verdammt, ein Produktivitätswunder zu brauchen, und kulturell darauf festgelegt, eines zu verhindern. Der 2019er-Beitrag fragte, ob KI eine nullte Welt schaffen könnte. Die Frage von 2026 ist nur noch, wer darin lebt, denn gebaut wird sie so oder so.

Sieben Vorhersagen für die nächsten sieben Jahre

Der 2019er-Beitrag hat sich sein Update verdient, indem er Behauptungen aufstellte, die scheitern konnten. Gleiche Regeln noch einmal: sieben Vorhersagen für 2033.

- Kein europäisches Frontier-Labor. 2033 operiert kein Labor mit EU-Hauptsitz auch nur innerhalb einer Größenordnung der Trainingsrechenleistung an der Frontier. Mistral endet übernommen, in Sovereign-Cloud-Verträge konsolidiert oder exzellent-aber-Nische.

- Feature-Verspätung ist keine Nachricht mehr. Dass Flaggschiff-KI-Produkte in der EU sechs bis vierundzwanzig Monate später, funktionsreduziert oder gar nicht erscheinen, wird Standardpraxis; mindestens ein prägendes Consumer-KI-Produkt der frühen 2030er erscheint schlicht nie im EWR, und niemand ist überrascht.

- Die Lücke erreicht die Statistiken. Das US-Arbeitsproduktivitätswachstum übertrifft das des Euroraums im Schnitt um einen vollen Prozentpunkt oder mehr, und die transatlantische Pro-Kopf-BIP-Lücke ist 2033 größer als heute; die ersten eindeutigen Nullte-Welt-Signaturen zeigen sich um 2030 in US-Sektordaten (Software, professionelle Dienstleistungen, Teile des verwaltungslastigen Gesundheitswesens).

- Europas KI-Sicherheitsschock. Vor 2033 wird ein großer europäischer Infrastruktur-Vorfall (ein Versorger, ein Klinikverbund, ein Behördensystem) auf eine Schwachstellenklasse zurückgeführt, die Organisationen der Glasswing-Liga auf ihren eigenen Stacks längst gefunden und behoben hatten. Die Antwort ist Notbeschaffung bei einem US-Labor: Souveränität per Rechnung.

- China kassiert die Deployment-Dividende. China führt bei Roboterdichte und Lights-out-Fertigung mit komfortablem Abstand, sein Open-Weight-Stack wird die Default-KI-Infrastruktur des Globalen Südens, und es wird die erste große Volkswirtschaft, die eine schrumpfende Erwerbsbevölkerung sichtbar mit KI plus Robotik in den offiziellen Statistiken ausgleicht.

- Deutschland adoptiert KI durch die Hintertür. Die Krise in Pflege, Verwaltung und Unternehmensnachfolge im Mittelstand erzwingt um 2029–2031 massenhafte KI-Adoption, auf importierten Stacks, schneller als jedes Digitalisierungsprogramm es je geschafft hat, und ohne dass ein einziges Strategiepapier wie geschrieben umgesetzt würde.

- Gigafabrik-Theater. EU-KI-Gigafabriken werden eingeweiht, mit Reden und Bändern; bis 2033 hat keine von ihnen einen Trainingslauf im Frontier-Maßstab beherbergt, und die gesamte öffentliche KI-Rechenkapazität der EU bleibt kleiner als der jährliche Zubau eines einzelnen US-Hyperscalers.

Wenn mindestens vier davon falsch liegen, hat Europa mich auf die bestmögliche Art überrascht, und niemand wird diese Bilanz lieber schreiben als ich.

Einige abschließende Gedanken

Ich beendete den 2019er-Beitrag mit dem Satz, dass wir, „um nachhaltigen Fortschritt zu ermöglichen, nicht nur aufmerksam sein, sondern den Einsatz dieser neuen Technologien vorbereiten und aktiv gestalten müssen“. Ich stehe zu dem Satz, mehr denn je, mit einem auf die harte Tour gelernten Zusatz: Gestalten setzt voraus, am Tisch zu sitzen.

Die nullte Welt ist kein Gedankenexperiment mehr; die Lücke zwischen ihr und der Ersten Welt öffnet sich in Echtzeit, in echten Zahlen, an echten Orten, in echten Fähigkeiten, in Memphis und Abilene und Shanghai. Vor sieben Jahren fragte ich, wie diese Lücke aussehen würde. Die ernüchternde Antwort von 2026 ist, dass Deutschland (und Europa) sich entschieden hat, „Reallabor“ zu sein und es empirisch herauszufinden, in Echtzeit… von der anderen Seite.

Comments